Rates, rates, rates. I'm sure you're tired of hearing the news about interest rates, right?

Well, earlier this year I predicted that rates were not going to go down as low as most people were predicting, and so far, it looks like that's what's happening. Here are a couple of recent key points from our friend Michael Leland over at Mortgage Trust.

- The Fed unanimously voted to keep rates unchanged at their FOMC meeting last week and are projecting that rates won’t go as low as previously projected in 2026 or even beyond.

- They were a lot more dovish/accommodating and still plan to cut rates (still likely 3 times). They just aren’t talking specifically about when we’ll see those cuts. Fed Chairman Powell made a comment about the recent inflation readings being a bump in the road, but not unexpected.

Remember, that just because the Fed cuts rates, does not mean that mortgage rates will directly or proportionately be cut as well. 30 year fixed rates are still in the high 6% range as of today.

SO with all that said, we're still encouraging our Buyer clients to negotiate for a temporary rate buy down if they are worried about their monthly payment at a higher rate. I mean, wouldn't it be nice to have a WHOLE interest rate point or TWO lower until these "cuts" do happen?

So, what does that look like, you ask?

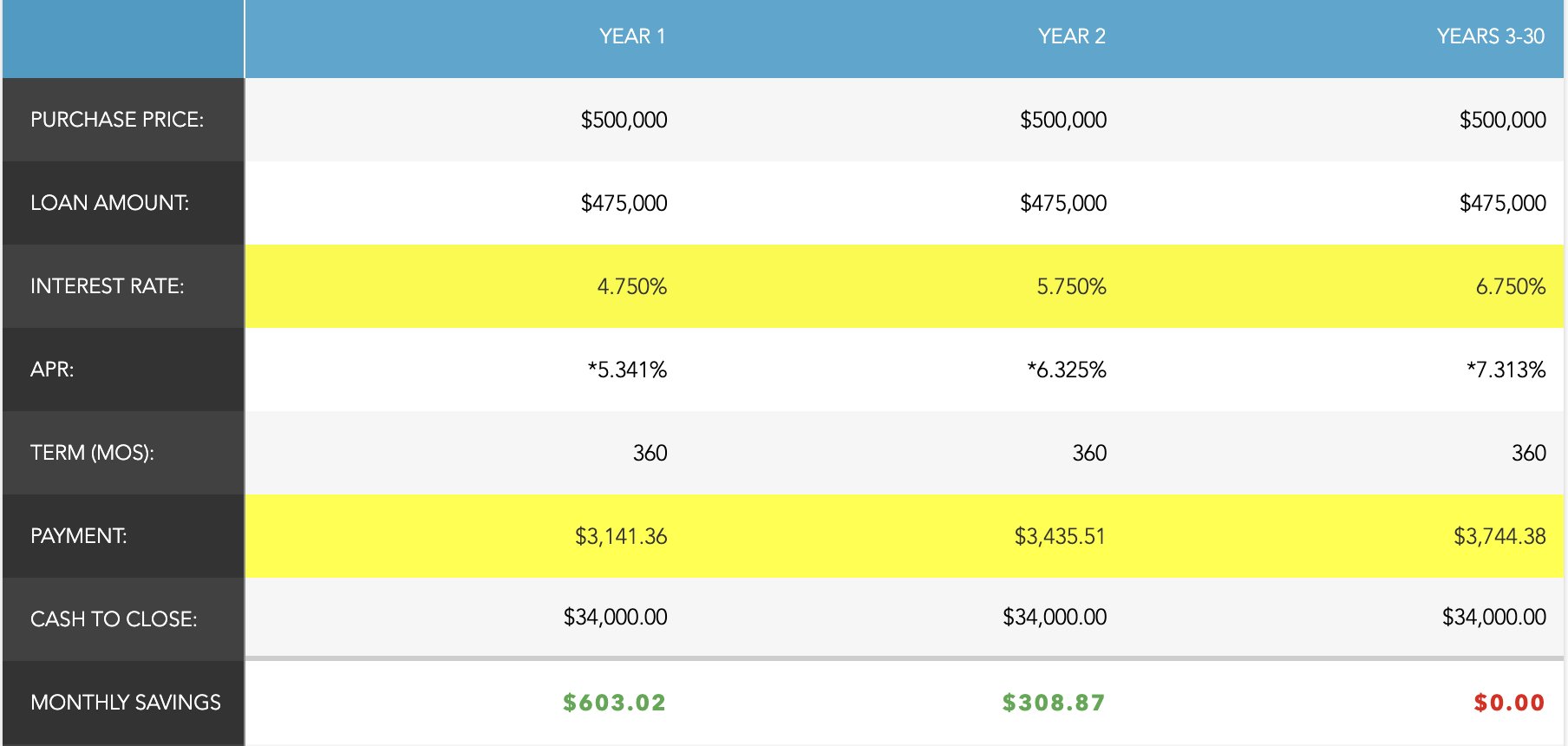

When you're writing an offer for a house, especially if you find a house that's been sitting on the market for a little while, we can potentially ask the seller to pay that difference in interest up front as a part of your closing costs.

Using the example of a $500,000 house purchase with $25,000 down and assuming a 6.75% interest rate, we would need the Seller to pay $10,944 up front which would give you a 2% better interest rate for the first year and a 1% better interest rate for the 2nd year. Which would make your 1st year's payments a whole $600/mo cheaper.

Using those same numbers, if we could only negotiate a 1 year rate buy down for a cost of $3,708 to the Seller, your payment would still be $308.87 cheaper per month.

Needless to say, there are options if you don't want to delay your home purchase. After all, home prices continue to steadily increase, and that doesn't look like it's going backwards any time soon.

Reply to this email if you'd like more information or clarification- we'd love to chat!

Amy, Kristine and Margo- The Place Portland Team